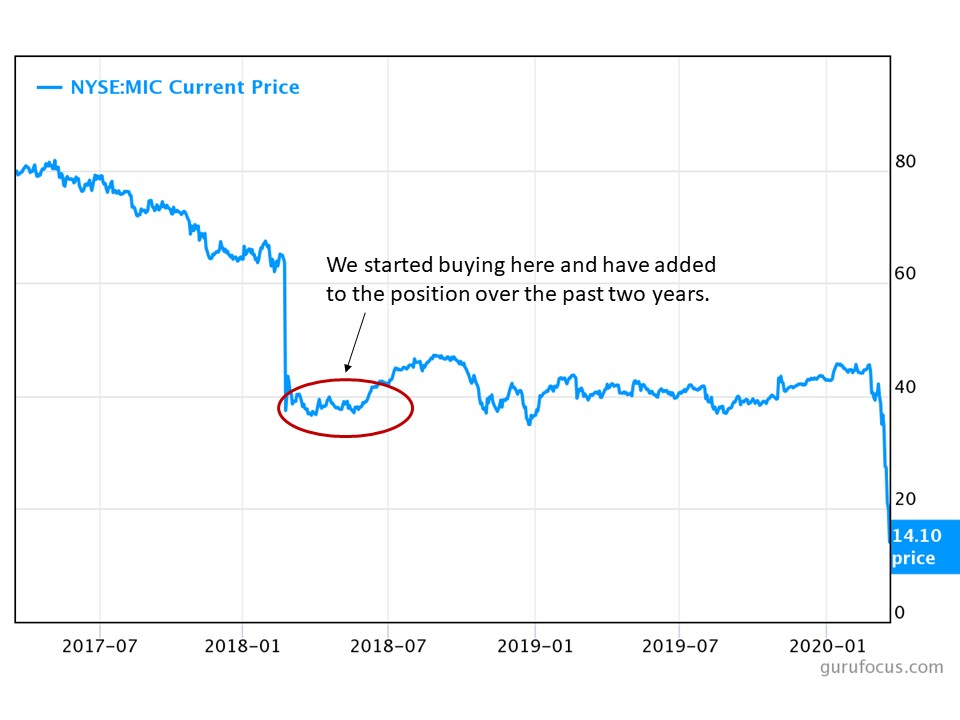

We’ve owned Macquarie Infrastructure Company (MIC) for about two years in our income-focused portfolios. It’s been a rough ride, to say the least, particularly over the past month.

Macquarie Infrastructure really fumbled its messaging when the company unexpectedly slashed its dividend in early 2018. By the time the dust had settled, the shares were was trading for less than half their 52-week highs.

The share price proceeded to trade in a fairly tight band around $40 per share for the following two years… and then the coronavirus panic hit, sending the shares into a tailspin losing two thirds of their value from recent highs.

The share price declines here aren’t entirely “irrational.” MIC is relatively thinly traded and has dependence on aviation. In an illiquid market, declines like these can happen. But they are excessive.

The biggest risk to MIC shareholders is that the dividend gets reduced or eliminated for a couple quarters. That happened during the 2008 meltdown, and it could easily happen again. But the underlying infrastructure assets are solid and, once life more or less returns to normal, will be back in demand.

MIC gets 90% of its earnings (EBITDA) from petroleum storage and aviation services, two segments that look particularly vulnerable today. Each provide about 45% of EBITDA. We won’t know for sure what the total damage will be to MIC until their quarterly numbers come out. But management did offer a little guidance yesterday.

Macquarie Infrastructure Corporation today announced that the performance of its businesses has been consistent with the Company’s expectations over the first ten weeks of 2020.

At International-Matex Tank Terminals (“IMTT”), market conditions have been supportive of the storage and handling of petroleum products. Utilization at IMTT is expected to increase to over 90% in April, up from 86% at year end 2019.

“IMTT has leased a substantial amount of storage capacity in the past two weeks, primarily distillate tanks at its Bayonne, New Jersey terminal with a weighted average term of over one year,” said Christopher Frost, chief executive officer of MIC.

General aviation flight activity, the primary driver of the performance of Atlantic Aviation, was stable during the period resulting in jet fuel sales being generally consistent with 2019.

“While the impact of COVID-19 on general aviation flight activity in the future is unclear, including as a result of government and corporate travel restrictions and the cancellation of sporting and other events, Atlantic has performed well during the period and remains focused on serving the needs of the general aviation community and operating safely and efficiently,” Frost said.

The memo was short of specific detail I would have liked to have seen, but a few things jump off the page. To start, the petroleum products storage business might actually benefit from the Saudi-led price war. In a supply glut, the excess has to go somewhere.

It’s the aviation services that are the big question mark. Revenues will plunge in that segment in March and April, and we don’t know when flight schedules will resemble anything “normal” again. Even if the virus disappeared tomorrow, there would be untold numbers of vacations and business meetings that would have been cancelled and not rescheduled.

So, what’s the aviation business worth? Let’s say for the sake of argument it’s worth zero. Literally nothing. Assuming MIC was fairly priced when it traded around $40… and I’d argue it was underpriced by at least $10 per share at that price… even with its aviation business worth zero, MIC should be trading at $22 per share. The stock closed yesterday at $14.10.

This would imply the aviation business is worth negative $8 per share, which is utterly ridiculous.

This is not an in-depth analysis. This is a quick-and-dirty, back-of-the-envelope reality check. I realize there are other concerns, such as debt service. The company carries about $3 billion in debt. And I think that it’s very possible that the company may ultimately need to trim back its dividend.

Still, when the stock was trading at less than half of book value and less than 0.75 times book value, it would seem that there’s a decent margin of safety, no matter what comes next.

Disclosure: Long MIC

[…] month I did a quick and dirty look at Macquarie Infrastructure, noting that “The biggest risk to MIC shareholders is that the dividend gets reduced or […]

[…] month I did a quick and dirty look at Macquarie Infrastructure, noting that “The biggest risk to MIC shareholders is that the dividend gets reduced or […]