As I wrote recently, mortgage REITs as a sector are trading at some of the steepest discounts to book value in their histories. I consider mortgage REITs trading at eighty to ninety cents on the dollar to be a fantastic bargain. But I also know that those bargains exist for a reason. With bond yields–and mortgage rates–scraping along near all-time lows and the Fed expected to at least modestly raise rates this year, the fear is that the interest rate spreads that allow mortgage REITs to pay out such large dividends are about to get crimped…and force the mortgage REITs to slash their dividends.

When mortgage REITs’ higher-yielding mortgages get prepayed by homeowners, the mortgage REITs are left with slim picking to reinvest in today’s market.

It’s a problem with an easy solution. Rather than buy low-yielding mortgages–or slide down the credit quality scale to chase yield–mortgage REITs trading at discounts to book value should repurchase their own shares. In fact, I’d argue it’s the only sensible solution at current prices.

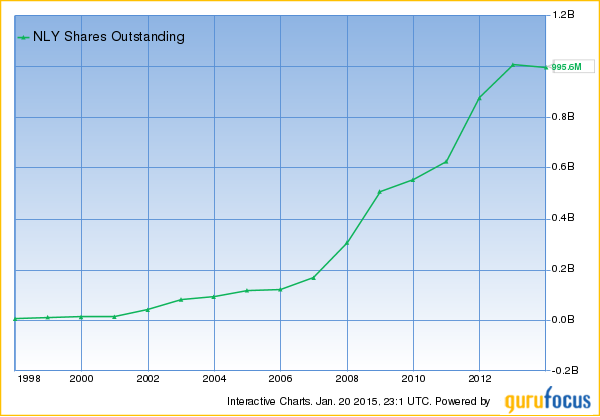

Mortgage REITs haven’t been very active on the share repurchase front. Annaly approved a share repurchase program in 2012, but it didn’t amount to a lot. Looking at Annaly Capital’s (NLY) history (see chart above), the REIT has been a lot more aggressive in issuing new shares. That made sense when interest rate spreads were wide and the high yields were there for the taking. But it certainly makes no sense at today’s prices. And to Annaly’s credit, they’ve moderated the new share issues of late.

Frankly, if Annaly–and the rest of the mortgage REITs trading at deep discounts to book value–care about the best interests of their shareholders, they will step up the share repurchases as their portfolios of mortgage securities roll off, by doing this, more people would want to get a mortgage loan. If you don’t buy your own stock at 80 cents on the dollar, then when would you?

Charles Lewis Sizemore, CFA, is chief investment officer of the investment firm Sizemore Capital Management and the author of the Sizemore Insights blog. As of this writing, he had no position in any security mentioned.

[…] late January, I suggested that mortgage REITs should aggressively repurchase their shares. Rather than buy low-yielding mortgages–or slide down the credit quality scale to chase […]