Why Invest in Alternatives?

You probably have a good grasp of why diversification is important. Throwing out the financial jargon, it essentially boils down to not putting all of your eggs in one basket. But it also gets a lot more sophisticated than that. Many investors feel that they have adequate diversification because their assets are spread across several stocks or mutual funds. And to an extent, they are right. Owning multiple stocks reduces the risk of downside from any single position.

But there is also a major problem with this: Correlation.

If Apple and Microsoft stock prices were to move together in lockstep, you wouldn’t be getting much in the way of diversification by owning both. And in a real bear market, virtually all stocks drop together.

True diversification means owning assets that do not move together. Investment A can go up, down or sideways, and it should have little or no impact on Investment B.

This is where the beauty of an alternative portfolio comes into play. A carefully constructed alternative portfolio will have assets that are minimally correlated to each other and to the stock market as a whole.

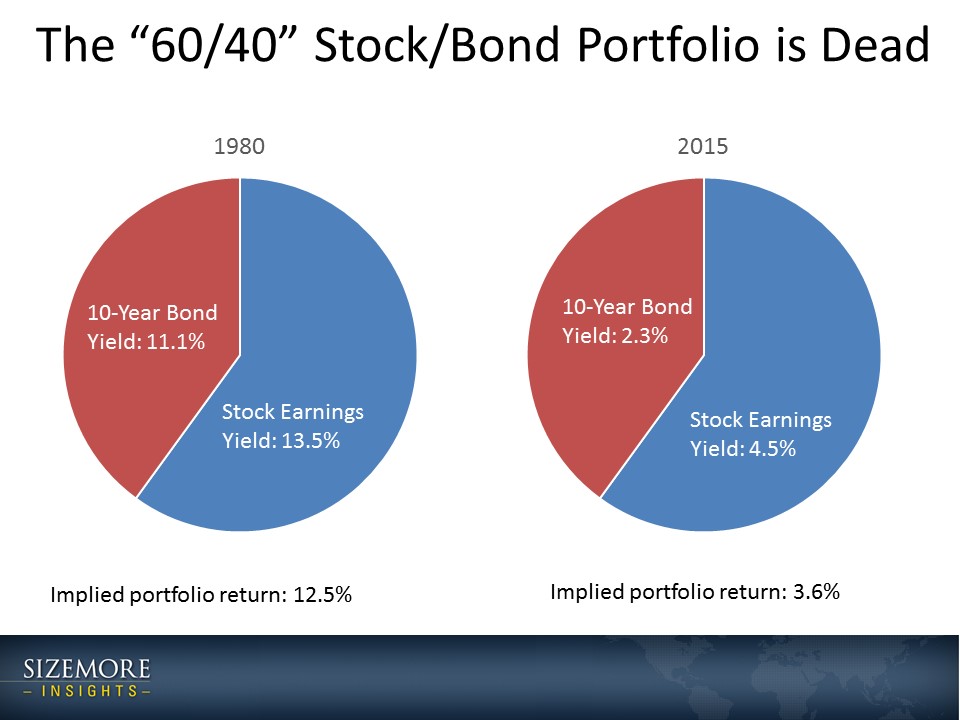

Why the 60/40 Portfolio is Dead

Alternative assets weren’t particularly popular in 1980. There is a reason for that. Back then, traditional bonds offered a respectable return. A blended 60/40 portfolio of stocks and bonds offered a solid expected return.

Flash forward to to present day. At current bond yields, investors will be lucky to get a 2% return in bonds. And compounding the situation, stocks are also expensive by historical measures and priced to deliver sub-par returns.

Accepting a traditional asset allocation is accepting the possibility for disappointing returns in the years ahead. If you want better performance, we need to look elsewhere.

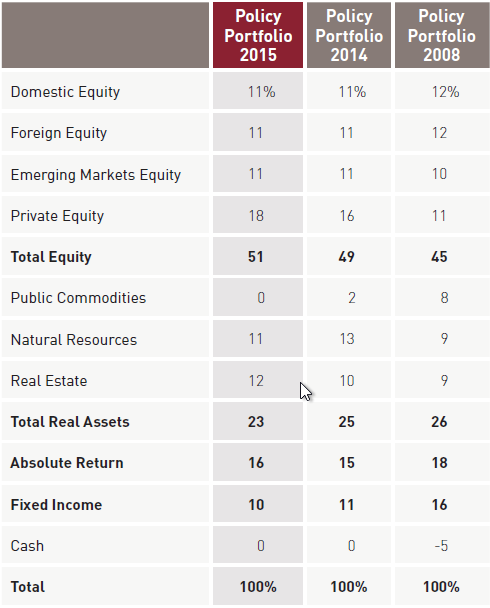

While ordinary investors have traditionally invested in stocks, bonds and CDs, wealthy investors and institutions have always had a broader allocation.Consider the case of the Harvard University endowment fund.

As of 2015, the Harvard endowment fund had only 33% of its funds in stocks. It has another 18% in private equity and 12% in real estate. The rest is spread across everything from timberland to absolute returns hedge funds. Let’s stop and ask an obvious question: If it’s good for trustees of Harvard, might it not also be good for you?

Not all of the alternative investments discussed will be appropriate for all investors. But we believe strongly that every investor can benefit from a proper allocation to alternative investments.

Charles Sizemore is the principal of Sizemore Capital Management.

If inflation is 13% in 1980, how much is the real rate of return for a 10 year bond in that year?

If inflation is 13% in 1980, how much is the real rate of return for a 10 year bond in that year?

[…] By Charles Sizemore, Sizemore Capital Management […]

[…] The 60/40 Portfolio Is Dead. Here Is Its Replacement January 12, 2016 […]

[…] wrote earlier this year that the 60/40 portfolio is dead. Well, rumors of its death were not greatly […]

[…] Harvard University endowment fund has famously kept about half of its portfolio in alternatives for years. It’s the particular choices of assets that the DPFP held that should have been a major red […]

[…] wrote earlier this year that the 60/40 portfolio is dead. Well, rumors of its death were not greatly exaggerated. The 60/40 portfolio that served retired […]

[…] Charles Sizemore, CFA and editor and portfolio manager for economic forecasting and investment research firm Dent […]